General economic conditions

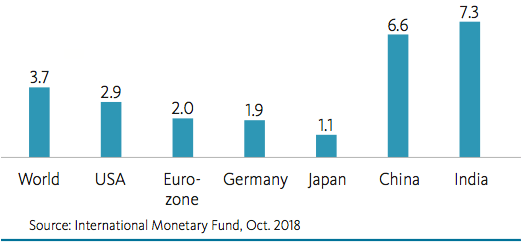

The global economy developed positively overall in fiscal year 2017/18. In its autumn forecast, the International Monetary Fund (IMF, www.imf.org) expects an increase of 3.7 % in global economic growth for 2018, only slightly below its spring forecast.

According to the IMF, the strongest growth momentum comes from Asia, especially China and India, and the US. However, the monetary authorities view the ongoing trade conflicts between the US and China as one of the biggest risk factors for global growth.

Expected GDP growth in 2018

in %

For the euro area, the IMF forecasts continued solid growth of 2.0 % for 2018, supported in part by Germany with predicted growth of 1.9 %. Both figures are somewhat lower than those the IMF outlined in its spring forecast. The IMF highlights high ongoing domestic demand with low unemployment numbers and the European Central Bank’s policy of low interest rates as key drivers of growth.

For the US, the IMF predicts economic growth of 2.9 % for 2018. Fiscal policy measures continue to be a significant reason for the good growth level there. The IMF sees the biggest risks for the American economy in the US government’s course – especially with respect to cooperation with China.

The Chinese economy should also continue to grow strongly in 2018. At 6.6 %, economic growth is expected to be at the level of the April estimate.

The global financial markets were mostly favorable in 2018. In the US, the Federal Reserve increased the federal funds rate multiple times during the course of the year. In September, it was at 2.00 to 2.25 %. In Europe, the European Central Bank maintained its zero interest rate policy but announced that it would end its bond-buying program at the end of 2018.